Introduction

HSAs in an Age of Uncertainty

Healthcare costs are taking up a growing share of workers’ wages (Tufts), premiums are projected to rise another 7% in 2025 (KFF), and inflation continues to erode real purchasing power. For working individuals and families, this economic instability makes it increasingly difficult to plan for the future—especially when it comes to managing the unpredictable cost of care. Add to that a political landscape defined by gridlock and volatility, and it’s no surprise that Americans feel like they’re on their own.

But buried within that uncertainty is a tool more consumers are turning to: the Health Savings Account (HSA).

Over the past two decades, HSAs have quietly emerged as one of the most effective, flexible, and resilient benefits available. Grounded in practicality, not politics, they’ve earned support from both sides of the aisle—including recent efforts to expand what they can cover. HSAs empower individuals to save pre-tax dollars, invest for the future, and manage rising care costs on their terms. In a divided system, they’re proving to be a unifying solution.

This report from Lively combines two proprietary data sets of account holder spending data from 2024 alongside healthcare consumer insights to reveal what economic indicators can’t fully capture: Americans are not just opening HSAs—they’re relying on them as a lifeline. Here’s what we found:

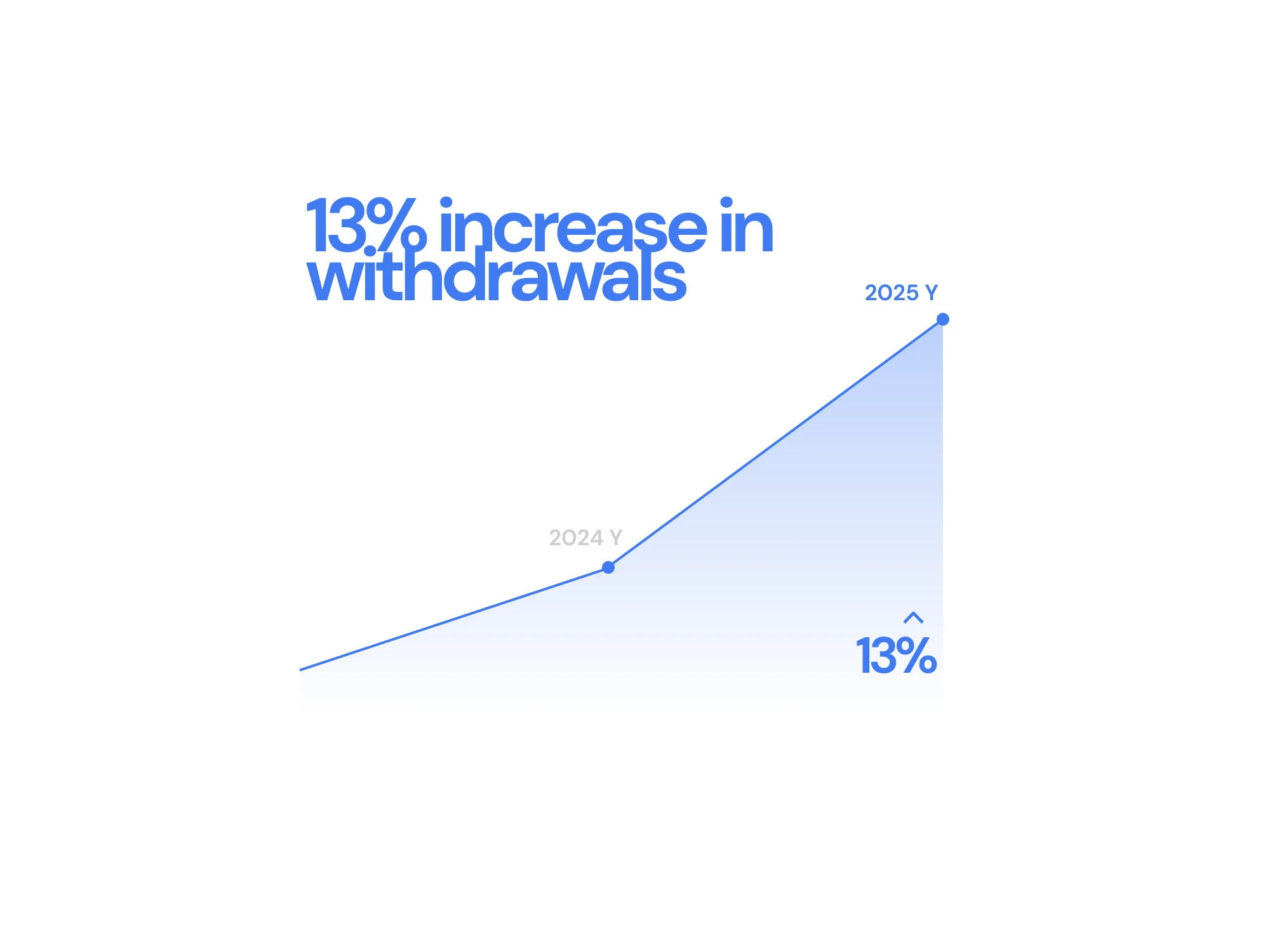

Withdrawals increased by 13% year-over-year.

Hospital spending rose 5% year-over-year.

And only 20% of HSA assets were retained, signaling that consumers are tapping into their savings to stay afloat.

Now, the recently passed One Big Beautiful Bill (OBBB) is poised to expand access even further. It introduces the most significant HSA reforms in nearly two decades. These changes, the majority of which are set to take effect beginning in 2026, modernize how HSAs are used and who can access them—signaling a broader recognition of the role HSAs can play in helping individuals manage care costs in a time of uncertainty.

The OBBB introduces a set of changes aimed at expanding both eligibility and flexibility for HSAs—bringing the benefit in line with the realities of how people access and pay for healthcare today:

Expanded HSA eligibility: Starting in 2026, individuals enrolled in Bronze or Catastrophic Affordable Care Act (ACA) plans will be able to open and contribute to an HSA. These lower-premium, higher-deductible plans were previously excluded due to HSA rules but will now qualify.

Permanent telehealth coverage: For plan years beginning after December 31, 2024, high-deductible health plans (HDHPs) that offer first-dollar coverage for telehealth will no longer be disqualified from HSA compatibility. This makes virtual care access a permanent, HSA-compatible benefit.

Inclusion of Direct Primary Care (DPC): Also starting in 2026, DPC arrangements (defined as arrangements costing up to $150/month for individuals and $300/month for families) are now recognized as qualified medical expenses under HSA rules—even if paid outside of a traditional insurance claim. Additionally, having a DPC arrangement no longer disqualifies you from funding an HSA.

These updates don’t just tweak the system; they recognize how consumers are actually using care today—digitally, outside traditional networks, and on tight budgets. And they give more Americans the ability to use HSAs as they were meant to be used: as adaptive, personally controlled financial tools.

Americans Are Feeling the Financial Squeeze

Across the country, working Americans are feeling the weight of the current economic climate. Stubborn inflation, shrinking incomes, and growing tariff concerns have made them more cautious and cost-conscious in terms of what they spend their money on. This has them rethinking healthcare expenses. Here are some sobering statistics from Lively’s research:

84% say healthcare costs are preventing them from reaching financial goals.

83% say these costs are making it difficult to save for retirement.

63% have skipped doctor visits, 59% have avoided treatment, and 56% have delayed or skipped medications due to cost.

One in four younger workers (ages 18–34) say they’ve been unable to buy a home due to healthcare expenses.

78% of employees say healthcare costs have delayed other major financial actions, such as saving for emergencies or paying off debt.

Americans are nervous about where they are financially and where the country is headed, and they are looking for solutions that aren’t undone with each election cycle. In response, Americans are rethinking value and are being intentional with every dollar they spend. They see wellness as a non-negotiable expense, but how they approach it is evolving. They want control over their healthcare spend so they can “make it count.”

Most employers will agree that employees skipping doctor visits isn’t a good thing. It’s not a good thing that employees aren’t taking needed medications or getting the treatment they need. And it’s detrimental to the health of the company that its employees are experiencing declining physical, mental, and financial health. Employees that don’t take care of their health experience higher rates of absenteeism and lower productivity while at work, and employees experiencing financial issues are more likely to spend work hours dealing with said issues (Gallup).

Employees need a better way to work within the system we have. They need more control over their spending, access to more affordable healthcare, and more ways to save money. And in order to feel comfortable adopting this solution, Americans need to have confidence it won’t be taken away or rendered unusable by the results of an election.

That’s why HSAs stand out for four powerful reasons:

They can be paired with Bronze/Catastrophic Plans from the ACA and High Deductible Health Plans (HDHPs) beginning for the 2026 plan year. These health insurance plans typically have the lowest monthly premium alongside other health plans offered and cover a long list of preventative care at 100% prior to the deductible being met.

The account belongs to the individual. That means employees—not employers, not insurers—control how and when funds are used. Employees control how much they save and for how long since HSAs aren’t bound by the same time constraints that affect other benefits like Flexible Spending Accounts (FSAs). If the employee leaves the company, or if they are no longer covered by an eligible health plan, they still retain access to their savings. This can increase employees’ comfort with saving money in their HSA.

HSA contributions receive a triple tax advantage. Employee contributions are tax-free, they grow tax-free and distributions for qualified expenses are tax-free even into retirement. This means employees can save up to 37% on the expenses for which they use these funds, making healthcare more affordable.

HSAs receive rare bipartisan support. In 2019, employers started covering more services under HDHPs at 100% pre-deductible. In 2024, a bill receiving bipartisan support codified this expansion. Now, in 2025, the passage of the OBBB cements expanded flexibility and eligibility further.

Whether covering routine doctor visits, unexpected emergencies, or planning decades ahead for retirement health costs, HSAs offer users complete autonomy over their healthcare dollars. It is money that, once set aside, is always available to them. It doesn’t matter what type of health insurance they have, if they leave their employer, or if their plan year has ended. It’s a new type of financial security which is a transformative shift in an environment where most financial decisions are out of the individual’s hands.

Despite the power of HSAs, their full potential remains underutilized. This is not due to a lack of interest but rather to a systemic education gap. Many Americans are not taught how to use HSAs strategically. As a result, key advantages—especially tax-free investing—are often left on the table.

This isn’t a shortfall of any single provider but a signal to the broader ecosystem: employers, brokers, HR leaders, and platform partners must work together to close this gap. Education must be treated not as an afterthought, but as a core feature of the HSA offering.

Employers, as the customer and one of the end-users of HSAs platforms, have an opportunity to demand a better system for their employees to use. And brokers and HSA platform providers should take note.

Five Strategic Actions Employers Can Take to Empower their Employees:

Bundle benefits thoughtfully. The starting point should be a benefits package built to support employees in the current environment. Pairing HSAs with LPFSAs (dental/vision), HRAs, and LSAs (wellness and lifestyle) reduces the impact of higher prices and encourages employees to take care of their physical health.

Choose a benefits provider with a modern platform that they control. To improve employee engagement with the benefits, the platform should be easy to access, include a mobile app, have a simple UX design, informative and real-time dashboards, and make account management efficient while having the ability to meet the consumer where they are without limitations

Choose a benefits provider that makes investing automatic and accessible. Features like first-dollar investing, lower thresholds, and auto-invest tools can radically increase adoption.

Prioritize year-round education. During open enrollment, education should focus on how these benefits work together to support employees through real-life scenarios. Throughout the year, employers should host mid-year check-ins and provide regular, seasonally relevant education materials that show employees how to best utilize the tools they have.

Contribute to employees’ accounts. HSAs that receive employer contributions, either in the form of seeded contributions or matching, have higher account balances than those that don’t receive employer contributions.

Conclusion

HSAs Are a Modern Safety Net For a Polarized Era

In a healthcare system often characterized by partisanship, complexity, and financial stress, HSAs are a rare bright spot. They offer real value, cross-party stability, and unmatched flexibility. They allow employees to pay for today’s costs and plan for tomorrow’s needs without the fear that their power will be diminished by the results of an election.

But to truly unlock the promise of HSAs, we must treat them not just as financial accounts, but as empowerment tools. That means better education, broader access, and smarter design—supported by employers, consultants, and benefit providers working in alignment.

America’s healthcare future may remain uncertain. But with the right strategies, HSAs can offer clarity, control, and confidence to millions of people today—and become the cornerstone of a benefits system that works for everyone.

FOR EMPLOYERS, BROKERS & HR TEAMS

Looking to offer Lively to your employees or clients?

Fill out this form, and we’ll be in touch within one business day.

Note: If you are an individual account holder or need personal support, please visit our Help Center.