The Lively Blog

SIGN UP FOR OUR

Newsletter

Stay up to date on the latest news delivered straight to your inbox

Do You Meet The Eligibility Requirements for an HSA?

Lauren Hargrave · August 26, 2020 · 5 min read

The value and benefits of an HSA are hard to pass up. You can choose to save for the short-term, long-term, or even retirement. And you have ultimate flexibility in when you open an account and how much you contribute. What isn't flexible are the eligibility requirements. Here’s how to determine if you’re eligible for an HSA.

Who can open a Health Savings Account?

To qualify for an HSA, you must meet the following criteria:

1. You’re covered by a qualifying High-Deductible Health Plan (HDHP).

2. The HDHP is your only health insurance coverage. Meaning, you don’t have supplemental coverage from a spouse or other family member (dental and vision is fine).

3. You don’t have or use a General Purpose FSA (Flexible Spending Account). But, you are allowed to have a Limited Purpose FSA for dental, vision, or a Dependent Care FSA.

Note: You can have an existing HSA and open an FSA. Your HSA funds will remain, but you cannot continue contributing to the health savings account.

4. No one else can claim you as a dependent on their tax return. 5. You’re 18 or older and not enrolled in Medicare (Part A and Part B) or Medicaid.

What is an HSA-eligible High Deductible Health Plan (HDHP)?

The IRS determines health plan eligibility on an annual basis. They adjust minimum deductibles and maximum out-of-pocket costs year-to-year for inflation and set different parameters for families and individuals. Additional requirements of HSA-eligible HDHPs: - Before any insurance payments kick in, an individual or family must pay for healthcare costs up to the deductible. This includes prescriptions. Preventative care is excluded from this definition. - Family coverage means having an insurance policy that covers the insured and at least one other person. Your health plan must meet all of these requirements to qualify as an HSA-eligible High Deductible Health Plan.

How much am I allowed to contribute?

Because the contributions you make to your account are tax-free, the IRS has strict rules about funding your HSA. Like the requirements around qualifying health plans, the IRS changes the amount you’re allowed to contribute to your HSA. This usually occurs annually and includes different HSA contribution limits for inviduals and families. If you or another member of your family is 55 or older you can contribute an additional $1,000 per year, called a "catch up contribution". Every contribution you make reflects a deduction in the amount of taxes you’ll pay on your gross income. You won’t pay taxes on your employer’s contributions either. But they will count towards your annual HSA contribution limit.

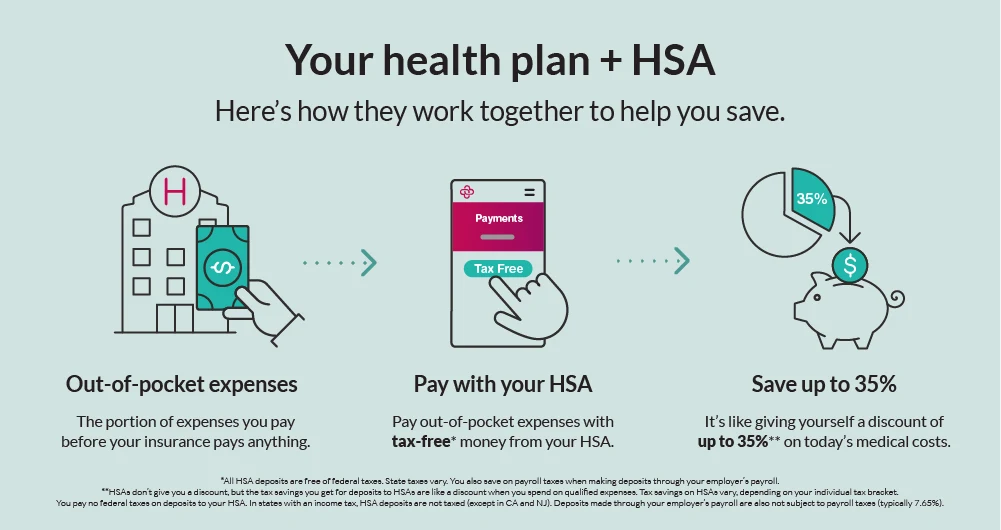

What expenses are eligible?

If you’re going to open an HSA, it’s fair to ask: how can I spend my money? The IRS refers to the expenses that you can use your HSA contributions towards as “qualified medical expenses.” These are always out-of-pocket medical expenses. Meaning, you can’t get a disbursement from your account for something your health insurance already paid for. Out-of-pocket medical expenses also exclude insurance premiums. Here are some of the expenses the IRS deems “qualified:” - Deductibles - Copays - Coinsurance - Diagnostic tests like x-rays, MRIs, blood tests, etc. - Medical supplies like bandages, braces, and crutches - Alternative medicine like acupuncture and acupressure - Prescription drugs - Over-the-counter drugs with a prescription - Quality of life enhancements like air purifiers (as long as you have a letter of medical need).

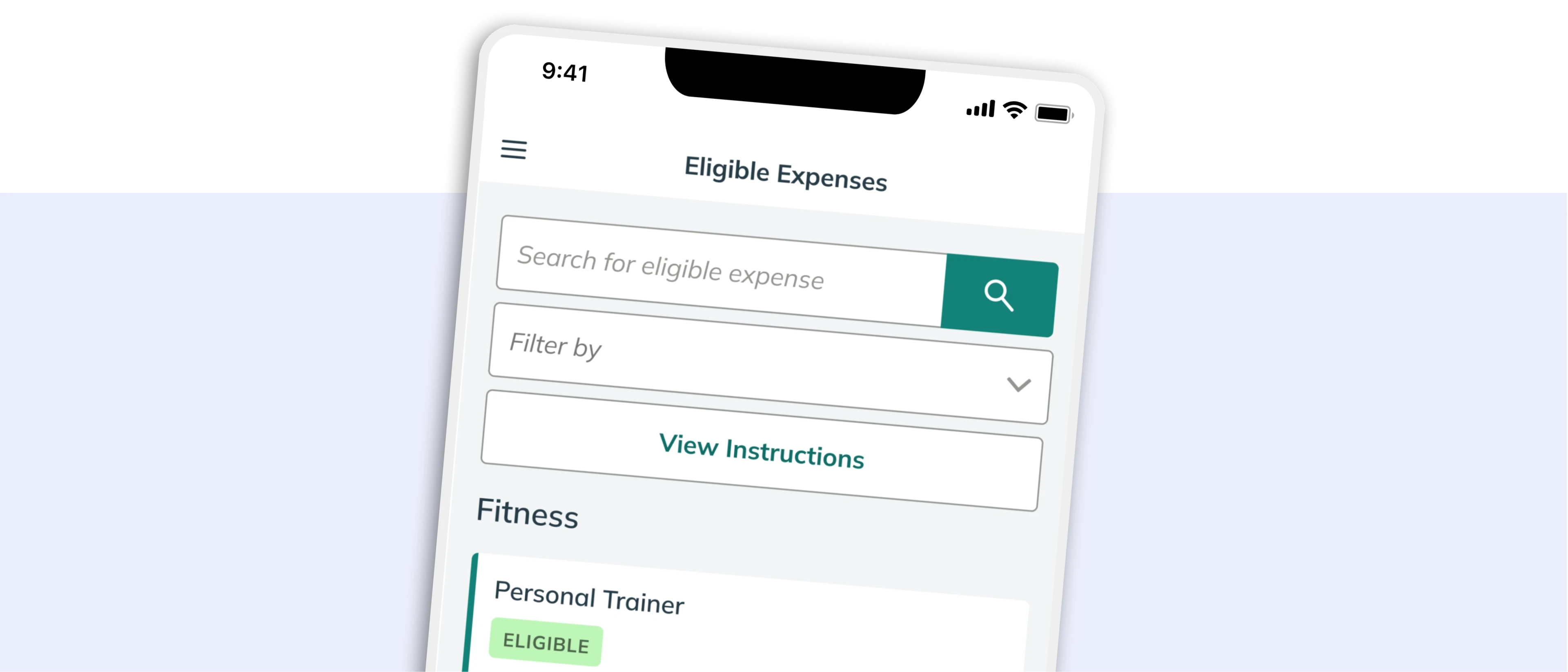

The IRS frequently updates its list of qualified medical expenses. So, if you’re not sure what you’re paying for is covered, check out our comprehensive list of HSA eligible expenses. Or, if you already have a Lively account, you can use the Eligibility Scanner feature on your mobile app to scan a product’s barcode and instantaneously determine whether or not it is eligible.

What happens when I lose my eligibility?

Circumstances like employment and health insurance needs can change in an instant. Here's what happens to your HSA if you no longer meet the eligibility requirements.

1. You own your account.

That means that if you change employers, become unemployed, or retire, you keep all contributions to that account. Even the contributions your employer made. So no matter your eligibility status, the money that has been contributed remains. And is available to you for distribution.

2. Lost eligibility?

As long as you’re under the age of 65, you can regain HSA eligibility. Once you regain eligibility you can continue making contributions to the same account. If it's available to you. Or you can open another account. If you’ve moved to a new employer that uses a different HSA administrator, you may have to roll the account from your previous employer into a new HSA. Or you can choose to keep two separate HSAs. HSAs offer a wide range of benefits, including tax advantages and a way to save for retirement, so it’s important to maintain your eligibility in order to maximize your savings.

Lauren Hargrave

Lauren Hargrave is a writer from San Francisco who focuses on technology, finance and wellness. She follows comedians like most people follow bands and believes an outdoor sweat session can cure almost any bad mood. She’s also been writing her first novel for so long, her mom doesn’t ask about it anymore.

Benefits

2023 and 2024 HSA Maximum Contribution Limits

Lively · May 16, 2023 · 3 min read

On May 16, 2023 the Internal Revenue Service announced the HSA contribution limits for 2024. For 2024 HSA-eligible account holders are allowed to contribute: $4,150 for individual coverage and $8,300 for family coverage. If you are 55 years or older, you’re still eligible to contribute an extra $1,000 catch-up contribution.

Benefits

What is the Difference Between a Flexible Spending Account and a Health Savings Account?

Lauren Hargrave · February 9, 2024 · 12 min read

A Health Savings Account (HSA) and Healthcare Flexible Spending Account (FSA) provide up to 30% savings on out-of-pocket healthcare expenses. That’s good news. Except you can’t contribute to an HSA and Healthcare FSA at the same time. So what if your employer offers both benefits? How do you choose which account type is best for you? Let’s explore the advantages of each to help you decide which wins in HSA vs FSA.

Health Savings Accounts

Ways Health Savings Account Matching Benefits Employers

Lauren Hargrave · October 13, 2023 · 7 min read

Employers need employees to adopt and engage with their benefits and one way to encourage employees to adopt and contribute to (i.e. engage with) an HSA, is for employers to match employees’ contributions.

Benefits

2023 and 2024 HSA Maximum Contribution Limits

Lively · May 16, 2023 · 3 min read

On May 16, 2023 the Internal Revenue Service announced the HSA contribution limits for 2024. For 2024 HSA-eligible account holders are allowed to contribute: $4,150 for individual coverage and $8,300 for family coverage. If you are 55 years or older, you’re still eligible to contribute an extra $1,000 catch-up contribution.

Benefits

What is the Difference Between a Flexible Spending Account and a Health Savings Account?

Lauren Hargrave · February 9, 2024 · 12 min read

A Health Savings Account (HSA) and Healthcare Flexible Spending Account (FSA) provide up to 30% savings on out-of-pocket healthcare expenses. That’s good news. Except you can’t contribute to an HSA and Healthcare FSA at the same time. So what if your employer offers both benefits? How do you choose which account type is best for you? Let’s explore the advantages of each to help you decide which wins in HSA vs FSA.

Health Savings Accounts

Ways Health Savings Account Matching Benefits Employers

Lauren Hargrave · October 13, 2023 · 7 min read

Employers need employees to adopt and engage with their benefits and one way to encourage employees to adopt and contribute to (i.e. engage with) an HSA, is for employers to match employees’ contributions.

SIGN UP FOR OUR

Newsletter

Stay up to date on the latest news delivered straight to your inbox