The Lively HSA

Open an HSA to pay for care and save on taxes

A health savings account (HSA) lets you set aside money for healthcare before it's taxed, so every dollar goes further. To open one, you need to be enrolled in a qualifying high-deductible health plan (HDHP). Once it's open, your contributions, growth, and withdrawals for qualified expenses all stay tax-free.

Use it for a doctor visit today, or let it grow for the costs still ahead. Either way, the Lively HSA is built to fit, with no monthly fees and no minimum to open. Unlike an FSA, your balance never expires and stays with you through job or plan changes. Choose to invest through a self-directed brokerage with Charles Schwab or a guided portfolio with Devenir, with no investment minimum on the guided option.

For Spenders

HSA spending, made simple

Your HSA isn't just for doctor visits. It covers thousands of everyday health expenses, often things you're already paying for out of pocket. Lively makes spending simple from the mobile app, so you always know what qualifies and where your money went.

With a Lively HSA, spenders can:

Cover everyday essentials like prescriptions, contacts and glasses, dental cleanings, sunscreen, and first aid supplies

Check if an expense qualifies before buying, right from the app

Pay directly with the Lively card at the pharmacy, the dentist, or online

Get reimbursed fast after paying out of pocket: snap a photo of the receipt and Lively handles the rest

Ask anything, anytime with the Lively AI Assistant, which gives straight answers based on your actual account

An HSA doesn't change what you buy, just what it costs you.

4.9 ★ mobile app rating

For Savers

Get ahead of future healthcare costs

Healthcare is one of the biggest expenses most people face, and much of it comes later in life. An HSA is one of the few accounts built for that reality: you get a tax advantage on every dollar you save for future healthcare, and starting early gives your balance more time to build.

With the Lively HSA, savers can:

Track your balance as it grows, so your progress is always visible

Set a contribution that fits your budget now and adjust it as your needs change

See how your HSA works alongside the rest of your coverage

Get personalized guidance so you're saving toward a real goal instead of guessing

You don't need a big balance to get started. Open an HSA with Lively, contribute what your budget allows, and let steady saving do the rest.

For Investors

Invest in Your Health

With Lively, you can invest from your very first contribution. There's no cash threshold to hit and no waiting for your balance to build, so your money starts working sooner.

As an investor, you can:

Start investing right away, with no minimum balance required

Choose how hands-on to be: pick your own investments through Charles Schwab, or go with a ready-made portfolio through Devenir that's managed for you

Get all three tax breaks in one account: contributions go in tax-free, gains grow tax-free, and withdrawals for qualified medical expenses come out tax-free

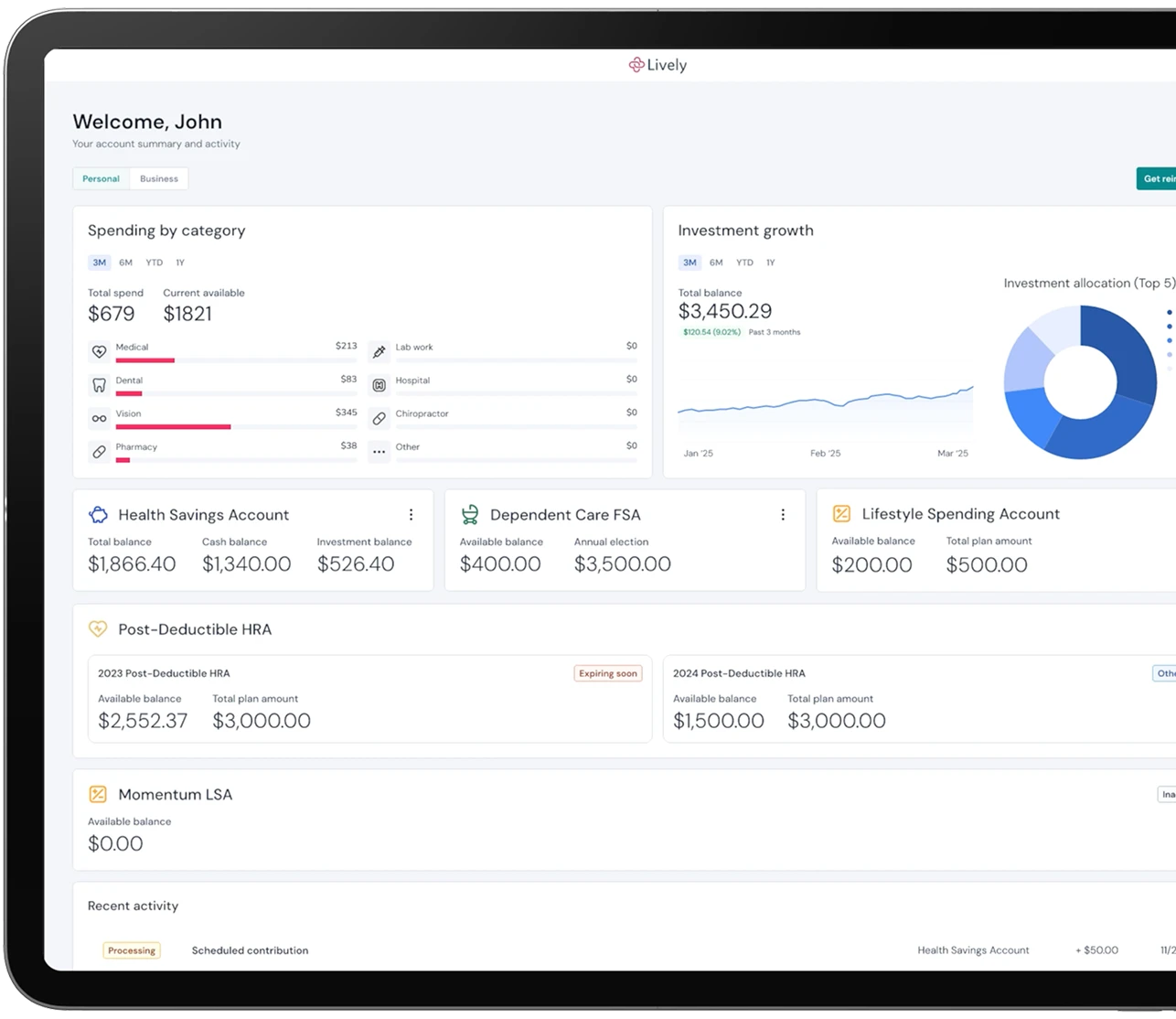

See your cash and investments side by side in one dashboard, on mobile or web

Every dollar you invest has years to grow, and all of that growth is yours tax-free.

Transparent HSA pricing. Zero hidden fees.

INDIVIDUALS

$0.00

Simple, transparent HSA pricing at last.

Free for individuals & families

HSA cash balance is insured and interest bearing*

Choose when and how to invest (optional - additional fee may apply)

BUSINESSES

$0.00

Per Employee Per Month (PEPM)

(Subject to a $200 monthly minimum)

Streamline HSA administration for less.

Intuitive dashboard administration

Effortless contribution management

Personalized investment options

* Lively is not an FDIC or NCUA insured financial institution. Lively partners with financial institutions in order to provide its products. These financial institutions are FDIC or NCUA insured and your HSA account may be eligible for pass through insurance. Certain conditions must be satisfied for pass-through deposit insurance coverage to apply. Please contact Lively for more detailed information.

Reviews

See why people choose Lively

Lively has been great! It's easy to submit reimbursement requests. Site is easy to navigate.

Reviews

See why people choose Lively

Lively has been great! It's easy to submit reimbursement requests. Site is easy to navigate.

Easy to use. Reimbursements came in a timely manner. So far no issue with the team or the app. Great support.

Lively is such an easy app to use. You can easily check an item's eligibility, use the debit card for eligible items, and easily process refunds! So easy to use this app, Lively makes having an HSA awesome!

For Employers

The HSA benefit that saves your team hours

Adding an HSA should make life easier for HR, not harder. Lively handles the administrative load, from contributions and payroll integrations to transfers and reporting, and keeps employees educated year-round. When questions come up, employees can ask Lively's AI assistant or talk to a real person instead of emailing your HR team.

95% of employers say they are satisfied with Lively.

Real numbers from real users

The numbers speak for themselves. Discover the trust, scale, and satisfaction behind the Lively HSA.

Lively Axis Platform

The platform behind a smarter HSA

Every Lively product runs on Lively Axis, an AI platform we built ourselves. That means it's designed for the people using it, and your HSA gets faster and better over time without you doing anything.

What that means for your HSA:

Changes to your account happen right away, not the next business day

Your whole account works from one system, so whether you're paying, filing a claim, or asking a question, nothing gets lost in between

New features and improvements show up automatically, with nothing to update

You never see Lively Axis working. You just notice your HSA runs smoother than it used to.

Features

Tools inside your HSA

Lively AI Agent

Ask a question and get a real answer based on your account, not a generic response. Available 24 hours a day for balance questions, eligible expenses, card issues, claims status, and reimbursement help.

Smart Claim

Snap a photo of a receipt. Lively reads it and files the claim. Valid claims are approved in seconds, and 94% are approved on the first try. If a claim needs review, a specialist handles it, so it is never auto-rejected.

Claim Sync

Connect your medical, dental, and vision plans, including a spouse's plan. Lively pulls the claims so they can track, organize, and reimburse them in one place. Works with 95% of US health insurance plans.

Eligibility Guidance

Find out instantly whether an expense qualifies. Answers come from IRS guidelines, not guesswork.

Smart Stacked Card

One card that works everywhere Visa is accepted, with Apple Pay, Google Pay, and Samsung Pay. Pay for eligible expenses directly from your HSA without filing a separate claim.

SERVICE

Real HSA support whenever you need it

HSA benefits questions don't always come up during business hours. The Lively AI assistant is available around the clock for fast answers. When you'd rather talk to a person, you're connected with someone who understands your account and can solve the problem.

The same support comes with every HSA, whether yours came through work or you opened it on your own.

93% of questions resolved in one conversation. No call center runaround.

HSA Resources

Tools and guides to help you get the most from your HSA

GUIDE

HSA Guide

Everything you need to know about how HSAs work, who qualifies, and how to make the most of yours.

Calculator

HSA Calculator

See how much you could save with an HSA, including your payroll tax benefit.

CALCULATOR

Loss Calculator

See how much time and money your team may be losing with your current HSA setup.

Tool

Eligible Expenses

A searchable list of qualified HSA medical expenses, so you always know what you can spend on.

Calculator

Compare Plans

Project your yearly costs under two health plans and see which one saves you more money overall.

Frequently Asked Questions (FAQ)

How do I open a Lively HSA?

You can open a Lively HSA online in just a few minutes through our simple, intuitive dashboard. Whether enrolling independently or through your employer's benefit program, the process is completely paperless. Once registered, you can securely link your bank account, set up contributions, and access your digital debit card.

Can I transfer my HSA from another provider to Lively?

Yes, you can easily transfer an existing HSA from another provider to Lively. We fully support electronic consent (e-consent) and e-signatures, making the process faster and reducing paper overhead. Your funds roll over securely without losing their tax-advantaged status, giving you full access on our modern platform.

How do I transfer my HSA to Lively from another provider?

To transfer your HSA, log into your modern Lively dashboard and initiate an individual transfer request. You will provide your current provider’s details and authorize the rollover using our secure e-consent process. For employer groups executing bulk transfers, Lively’s dedicated Customer Success team coordinates directly with the incumbent provider.

Can I open an HSA on my own without my employer?

Yes, you can open a Lively HSA on your own completely independent of your employer. Because health savings accounts are individually owned, you maintain full control over your funds, contributions, and investments. Your account features our modern user experience and remains free of monthly maintenance fees even without employer sponsorship.

Can I open a Lively HSA if I'm self-employed?

Yes, if you are self-employed and enrolled in a qualifying High-Deductible Health Plan (HDHP), you can open a Lively HSA. It provides an excellent way to save on payroll and income taxes while building a dedicated, tax-free fund for medical expenses and long-term health investments.

What fees does Lively charge for an HSA?

Lively charges $0 in monthly maintenance, opening, or closing fees for individual accounts. While the baseline account is entirely free for day-to-day saving and spending , choosing to activate optional investment features may introduce a small fee of $2 a month depending on your balance.

What happens to my Lively HSA if I change jobs?

If you change jobs, your Lively HSA stays with you for life because it is an individually owned account. You keep all your saved funds, and Lively continues to charge $0 in monthly maintenance fees. You can seamlessly continue using your card and investing without any hidden penalty fees.

How do I spend the money in my Lively HSA?

Lively gives you a Smart Stacked Card that works everywhere Visa is accepted, including Apple Pay, Google Pay, and Samsung Pay. You can also pay out of pocket and reimburse yourself through the Lively app. There is no deadline to reimburse yourself for past qualified expenses.

Which HSA lets me invest with no minimum balance?

Lively lets you invest your HSA with no minimum balance required. Choose a self-directed brokerage through Charles Schwab for hands-on investing, or a guided portfolio through Devenir with no investment minimum. Every dollar invested grows tax-free and withdraws tax-free for qualified medical expenses.

Can I invest my HSA with Lively?

Yes, you can invest your HSA funds with Lively using our two industry-leading options: Schwab and Devenir. We offer a choice of first-dollar investing with no minimum balance requirements. You can track, monitor, and manage your entire investment portfolio performance directly from your unified Lively web or mobile dashboard.

Can I open an HSA mid-year if I switch to an HDHP?

Yes, you can open an HSA with Lively as soon as your HSA-eligible high-deductible health plan coverage begins, at any point in the year. Your contribution limit is prorated based on the months you were eligible. Under the IRS last-month rule, being covered by December 1 may allow you to contribute the full annual limit.

Can I use my HSA for family members?

You can use your HSA to pay for qualified medical expenses for your spouse and anyone you claim as a tax dependent, even if they are not covered by your health plan. Their expenses are reimbursed tax-free just like your own. You cannot use it for adult children who are on your health plan but no longer your tax dependents.